Why financial jargon is preventing true financial inclusion

In the financial services industry, language is more than just a tool for communication, it is a gatekeeper.

For many consumers, especially in the South African market where financial inclusion remains a critical challenge, the biggest barrier is not only access to products but understanding them. Policies, investment documents and adviser conversations are often filled with technical terminology that feels foreign, intimidating and, at times, exclusionary.

The result? People disengage or worse, they make decisions they do not fully understand.

Financial services have evolved in complexity; driven by regulation, risk modelling, product innovation and evolving technology such as the use of artificial intelligence. While this precision serves a purpose of introducing higher levels of accuracy and simplification, it has also created an unintended complexity to the client resulting in a consequence of a language gap between the industry and the everyday person.

Research consistently shows that financial literacy plays a critical role in enabling people to access, use and benefit from financial services effectively. Yet literacy does not only cover knowledge, it is also meant to provide clarity. When language becomes a barrier, it directly undermines participation.

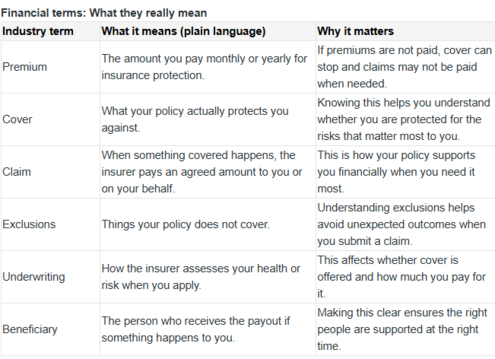

Terms like “beneficiary”, “underwriting” or “exclusions” are considered standard in the industry, but to the average person, they can feel overwhelming and abstract. Financial jargon, while efficient for financial professionals, often excludes those who need financial guidance the most.

In many cases, misunderstanding does not show up at the point of sale, however, shows up later when a claim is declined or a policy lapses. Confusion often stems from complex terminology, rushed explanations and product-heavy discussions, leaving people unclear about what they have committed to, this means them understanding what they are covered for, when they are not, the role and responsibility of the financial services provider.

This can be labelled a communication issue; however, it is a trust issue and ultimately becomes a participation issue.

What to do

Avoiding jargon starts with a deliberate shift in responsibility. Clear communication cannot be treated as a marketing preference or an adviser skill. It must be embedded across the organisation, from product design and legal drafting to member communication and claims interactions. This means testing language with real people, not only compliance teams, and asking a simple question at every stage: “would a non-specialist understand this without explanation?”. Where technical terms are unavoidable, they should be clearly defined using plain language and real-life examples that explain why the term matters to the individual.

Clarity also requires consistency and patience. Advisers and service teams should be supported with tools, training and time to explain concepts properly, rather than relying on dense documents or rushed conversations. Written communication should prioritise structure, clear headings and short sentences over volume and complexity. Importantly, understanding should be checked, not assumed. Encouraging questions, repeating key information and reinforcing messages across multiple touchpoints helps ensure that understanding carries through from onboarding to claims, where clarity matters most.

Financial inclusion is defined as the ability for individuals to access and effectively use financial services to build wealth and stability. But access without understanding is not true inclusion.

Participation requires confidence. And confidence requires clarity.

The way forward: Simplicity is the responsible thing to do

The financial services industry is at an inflection point. Products are becoming more sophisticated but consumers are demanding more transparency, simplicity and ease.

The opportunity is clear; those who master clarity will build trust. Those who build trust are more likely to earn sustained participation.

Simplicity does not mean reducing rigour or compromising accuracy. It means translating complexity into language that people can understand and act on with confidence. When individuals understand their financial choices, they make better decisions, remain engaged for longer and experience greater peace of mind.

Leave a Comment